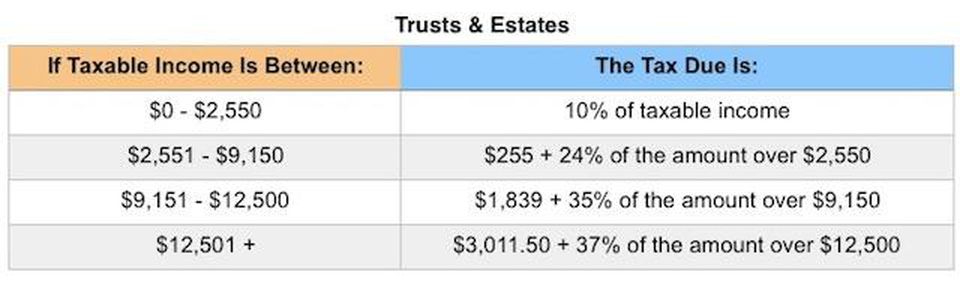

Estate & Gift Taxes

Estate Tax

The Estate Tax is a tax on your right to transfer property at your death. It consists of an accounting of everything you own or have certain interests in at the date of death (Refer to Form 706 (PDF)). The fair market value of these items is used, not necessarily what you paid for them or what their values were when you acquired them. The total of all of these items is your "Gross Estate." The includible property may consist of cash and securities, real estate, insurance, trusts, annuities, business interests and other assets.

Once you have accounted for the Gross Estate, certain deductions (and in special circumstances, reductions to value) are allowed in arriving at your "Taxable Estate." These deductions may include mortgages and other debts, estate administration expenses, property that passes to surviving spouses and qualified charities. The value of some operating business interests or farms may be reduced for estates that qualify.

After the net amount is computed, the value of lifetime taxable gifts (beginning with gifts made in 1977) is added to this number and the tax is computed. The tax is then reduced by the available unified credit.

Most relatively simple estates (cash, publicly traded securities, small amounts of other easily valued assets, and no special deductions or elections, or jointly held property) do not require the filing of an estate tax return. A filing is required for estates with combined gross assets and prior taxable gifts exceeding $1,500,000 in 2004 - 2005; $2,000,000 in 2006 - 2008; $3,500,000 for decedents dying in 2009; and $5,000,000 or more for decedent's dying in 2010 and 2011 (note: there are special rules for decedents dying in 2010); $5,120,000 in 2012, $5,250,000 in 2013, $5,340,000 in 2014, $5,430,000 in 2015, $5,450,000 in 2016, $5,490,000 in 2017, $11,180,000 in 2018, and $11,400,000 in 2019.

The new law doubles the amount that can be left to heirs tax-free in 2018, to about $11 million for singles and about $22 million for married couples. The amount will rise each year to keep up with inflation.

But, as with many changes in the law, this one expires at the end of 2025, when the tax-free amount will revert to earlier levels.

The law does not change the rule that “steps up” the basis of inherited property to its value on the date the benefactor died. As in the past, any appreciation during the life of the previous owner becomes tax-free.

When to File

Generally, the estate tax return is due nine months after the date of death. A six month extension is available if requested prior to the due date and the estimated correct amount of tax is paid before the due date.

The gift tax return is due on April 15th following the year in which the gift is made.

For more information please see IRS link: https://www.irs.gov/businesses/small-businesses-self-employed/estate-tax

Gift Tax

The annual exclusion for 2018 is $15,000

The gift tax is a tax on the transfer of property by one individual to another while receiving nothing, or less than full value, in return. The tax applies whether the donor intends the transfer to be a gift or not.

In other words, if you give each of your children $11,000 in 2002-2005, $12,000 in 2006-2008, $13,000 in 2009-2012 and $14,000 on or after January 1, 2013, the annual exclusion applies to each gift. The annual exclusion for 2014, 2015, 2016 and 2017 is $14,000. For 2018, the annual exclusion is $15,000

Gift tax is not an issue for most people. The person who makes the gift files the gift tax return, if necessary, and pays any tax. If someone gives you more than the annual gift tax exclusion amount ($15,000 in 2018), the giver must file a gift taxreturn. That still doesn't mean they owe gift tax.

What is the gift tax rate? If you're lucky enough and generous enough to use up your exclusions, you may indeed have to pay the gift tax. The rates range from 18% to40%, and the giver generally pays the tax.

Exemptions and tax rates

| Year | Exclusion Amount | Max/Top tax rate |

|---|---|---|

| 2018 | $11.18 million | 40% |

| 2017 | $5.49 million | 40% |

| 2015 & 2016 | $5.45 million | 40% |